Treasury Management in DeFi: Magic of Fixed Income

DeFi has seen protocol treasury values soar during the 2020/21 bull run. With the hype of the super-cycle, establishing prudent treasury…

DeFi has seen protocol treasury values soar during the 2020/21 bull run. With the hype of the super-cycle, establishing prudent treasury management practices has been of low priority.

However, the market has shifted. With the recent downturn, protocols and DAOs need to start thinking intentionally about runway preservation in practice, especially with a few protocols already performing layoffs and a reduction in compensation for contributors.

Comparing and contrasting the asset value of top treasuries a year ago vs. what they are now, we observe dramatic drops in treasury value.

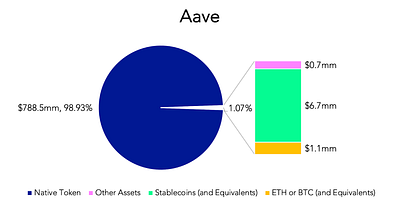

AAVE:

AAVE’s treasury value has gone from $1.08B in August 2021 to $101M in July 2022.

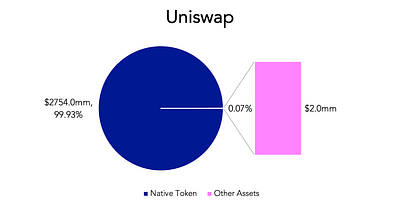

Uniswap:

Uniswap’s treasury value has gone from $4.8B in September 2021 to $1.3B in July 2022.

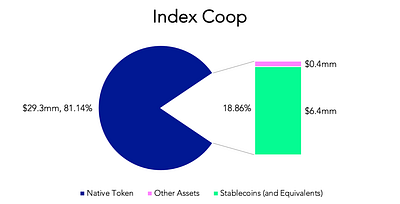

Index Coop:

Index Coop’s treasury value has gone from an ATH of $105M in September 2021 to $4M in July 2022.

DAOs need to start structuring treasuries in a sustainable way that hedges against volatility of broader crypto markets. Yet, the majority of DAO treasuries are composed nearly entirely of a protocol’s native token.

In “A New Mental Model for Defi Treasuries” author Hasu explains that these native tokens are not actually assets on the balance sheet, but are instead “the crypto-equivalent of authorized but unissued shares.”

This is a recipe for disaster. A downturn market can dramatically deflate native token prices, creating financial pressure where DAOs could be forced to sell these “unissued shares” to meet demands. These sales would only further depress the token price and the treasury value in turn.

If DAOs remain over-indexed on their native tokens, this will leave treasuries at high risk, extremely exposed to fluctuating market conditions.

DeFi can learn from TradFi Experience

DAO asset and treasury management is a nascent application of an age-old problem. Its implementation in DeFi has been driven by hype, experimentation, and unstructured short-term thinking.

TradFi treasury management practices offer a wealth of existing, time-tested knowledge the DeFi space can leverage.

Our industry tends to have a bias to hubris, but DeFi can and should learn from the experience of others. Doing so introduces a two-way flow of information in which Tradfi players are more open to learn from and engage with DeFi as well.

Starting with: what has made for good treasury management strategies in TradFi? How are institutions currently thinking about asset diversification in the real world? Where can we spot parallels useful in crypto? Where are the differences?

Treasury management in DeFi has, thus far, been driven by shots in the dark. Answering these questions allows us to bring treasury management to the light, in a much more systematic and professional way.

Existing Treasury Management Practices

Treasury portfolio construction is a deeply academic and conservative approach.

Institutions start with a clearly defined investment mandate, which outlines what their treasury’s purpose is and establishes a set of investment principles that drive how much risk the organization is allowed to take.

Typically the investment principles (ranked in order of priority) are:

- Liquidity (having cash on hand)

- Capital Preservation (chance of losing money)

- Return

Strategy is shaped around investment principles and their order of priority (e.g. don’t increase return if it comes at the risk of capital preservation, and always emphasize on a near zero chance of losing money).

Without some kind of guidance of what the investment mandate looks like, it’s difficult for the community to create a treasury proposal, and near impossible to conduct responsible, measured treasury management.

This becomes especially critical in cases of contradicting proposals or community disagreements on how to allocate the treasury.

Each DAO should construct their own investment mandate, and determine their own investment principles.

Having a mandate for the community to reference — “what should this parameter look like, where are we optimizing” — gives the community a structured, long-term strategic way to plan, submit proposals, vote, and proceed.

How Institutions Structure Investment Mandates

Each DAO/Protocol ought to begin by 1. defining what their treasury’s purpose is, and 2. what guidelines to follow.

The questions DAOs need to ask themselves to establish these rules are:

- What are your risk metrics? How much risk are you allowed to take?

- What types of risk can you be exposed to?

- What types of risk can you *absolutely not* be exposed to? How do you minimize that exposure?

- How do you hedge against unjustified risk?

- What assets are you allowed to invest in? Which stables? What is the risk of each? What is the implied risk? Can you short? Are you allowed to short? Are you long?

- Which assets should you minimize exposure to?

- How much of your portfolio needs to be liquid?

- Which terms?

The art of good portfolio construction lies in a functioning investment mandate, and clearly defined portfolio weights that break down risk exposure.

Before optimizing for return, a treasury manager must guarantee all risks are accounted for.

How? Begin by a traditional plotting of expenses. This exercise allows a DAO to determine how much of the portfolio needs to be liquid.

When it comes to treasury management, liquidity — how much “cash” on hand to support the business — is the number one priority.

Maintaining liquidity requires a disciplined exercise in cash flow management:

- Write down every outflow

- Match it with an inflow

Unmatched outflows will eat into your working capital. You want your working capital to remain at a set minimum

- e.g. only dips below if a trade fails and there is a mismatch of cash flows

Known payments should be plotted in a spreadsheet:

- Recurring: salaries / subDao / working group payments

- Big spends: service provider (hire a MM), M&A (Fei + Rari)

- Have working capital maintained at a minimum

Only once these knowns are established, can the community go about tailoring a treasury management strategy.

Element and the Magic of Fixed Income

Fixed income is a tool highly underutilized in DeFi, but almost perfectly tailored to the needs of treasury managers.

Element Finance, an open source protocol for fixed yield, actively thinks about creating markets and assets that fit the conservative mandates necessary for successful treasury management.

Element’s principal tokens have innate characteristics that make it easy for treasury managers to adjust to their personal mandates.

1. Liquidity Risk

Element Protocol is designed to optimize for liquidity allowing users to exit their position at any time, while still enabling users to gain yield until they decide to exit.

2. Capital Preservation

Asset diversification in DeFi doesn’t work when you deposit into curve pools. Any pool that does an x*y curve for the AMM, creates the opposite of diversification — if any one of those assets go to 0, it all goes to 0.

What if the market is in a downturn?

In the case of bear markets, why run the risk of a market sell when you can lock it in now by buying a fixed asset that offers 100% certainty.

In the example of Terra — the price wasn’t there when it was needed the most. Protocols will find the same thing with their treasuries in the bear market

Fixed maturity dates offer a big advantage over assets that don’t mature.

The benefits of an asset with a fixed maturity date include:

a. At maturity, it acts as a costless liquidation

b. Saves you one round trip of transaction costs

c. Perp, equity, long-dated maturities, staked position => go and market sell.

Incurs loss: gas fee (fixed fees) + bid-ask (slippage) + price move (in crisis it’s down => wrong-way risk)

When one of Element’s pools matures at the end, it matures at 1. You’re not exposed to slippage when you go to withdraw that money, as the market is closed.

3. Cash Flow Management

The magic of fixed income especially comes into play when looking at cash flow management.

Only fixed interest rates offer the certainty necessary for budget and financial planning.

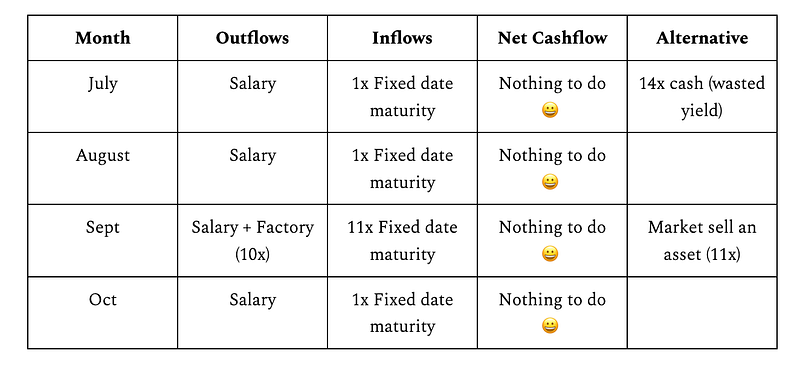

After knowing what expenses you may have to pay out in the next 3–6 months, with Element’s fixed rates one can strategically time investments into pools whose maturity dates land on months with disproportionately higher outflows.

Treasury managers can play around with fixed date maturity to line up greater inflow on months with high expected outflows. This allows protocols to look out 12 months ahead and strategically match fixed rates of return to cover expenses.

Timing is frequently cited as the most important strategy consideration in successful treasury management. Element’s lock-ups solve for time factors.

Conclusions:

In Introducing Element’s Treasury Management Initiative Element COO Charles St.Louis wrote, “Our goal is for asset managers to be able to take a passive long-term strategy with minimal exposure to interest rate risks and incrementally grow the size of their treasury using Element.”

He explains that using fixed rates instead of variable rates “allows Element to provide structured, reliable, and predictable capital growth, even within the volatile market that governs the DeFi space, while maintaining capital efficiency.”

Fixed income is one of multiple DeFi tools that can be used to bring much-needed structure to treasury management — a thus ignored but highly critical part of any thriving financial ecosystem.

Acknowledgments and special thanks to Mihai Cosma, Windra Thio, Giovanni Fong, Linda Xie, Charles St.Louis, and Alim Khamisa for the conversations and feedback! And a thanks to Yuan Han Li for lending the use of his graphs.